Reports

Our reports combine rigorous technical exploration with objective market validation. We pull the critical insights you need to pressure-test your core assumptions, minimize downside risk, and identify true product differentiation before spending capital on infrastructure or scale.

-

Free Market Overviews & Demand Signals

Immediate access to baseline sector tracking, high-level industry benchmarks, and foundational consumer behavior shifts.

-

Premium Deep-Dives & Go-to-Market Frameworks

Exhaustive, niche-specific intelligence packages containing proprietary data validation, architectural stress-testing insights, and granular competitive alternatives analysis.

%20(2)_page-0002.jpg)

Free

FMCG Consumption Trends Across Tier 1, 2, 3 Markets in India

The Indian FMCG sector is undergoing a structural shift, with volume growth (6.5%) becoming the dominant driver of expansion, reflecting a strong recovery in consumer demand. This growth is geographically inverted: Rural markets now lead with 7.7% volume growth, nearly doubling the urban rate. Tier 2 cities are the "Sweet Spot," exhibiting the highest consumption volume per household. While metros face saturation, Tier 2 and Tier 3 markets are leveraging digital access for aspirational e-commerce. You will get a PDF (4MB) file

Free

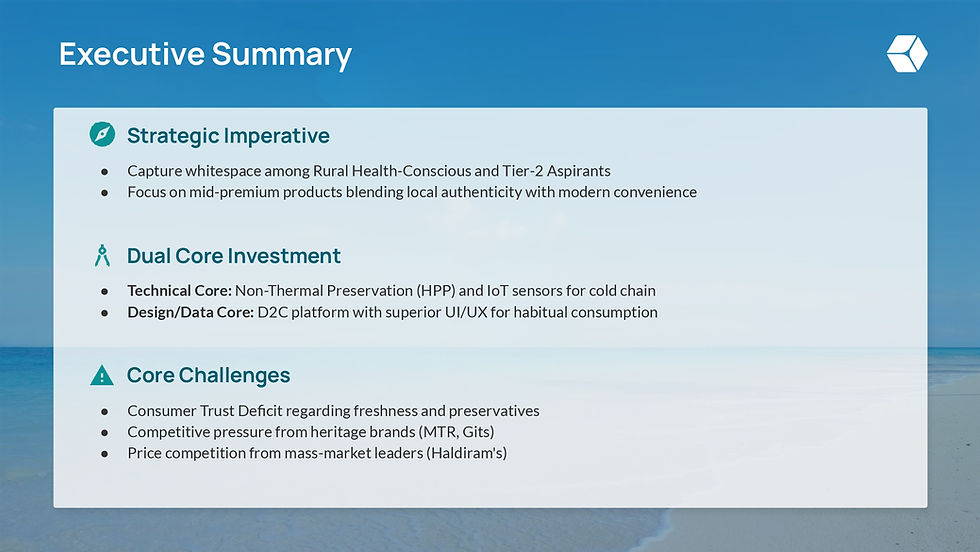

Competitive Whitespace in FMCG Brands in India

The Indian Ready-to-Eat (RTE) market is set for 16.4% CAGR growth despite a significant consumer trust deficit regarding freshness and preservatives, and intense competition from established brands. The key strategy is targeting Rural Health-Conscious and Tier-2 Aspirants with mid-premium products that balance local flavors and modern convenience. Technical Core: Investment in Non-Thermal Preservation (HPP) for clean-label products and sensors for verifiable cold chain resilience. Design/Data Core: A Direct-to-Consumer (D2C) platform with superior UI/UX to drive high-margin habitual sales. Success hinges on overcoming competitive price erosion by investing 15–25% of revenue in brand-building. You will get a PDF (5MB) file

$47

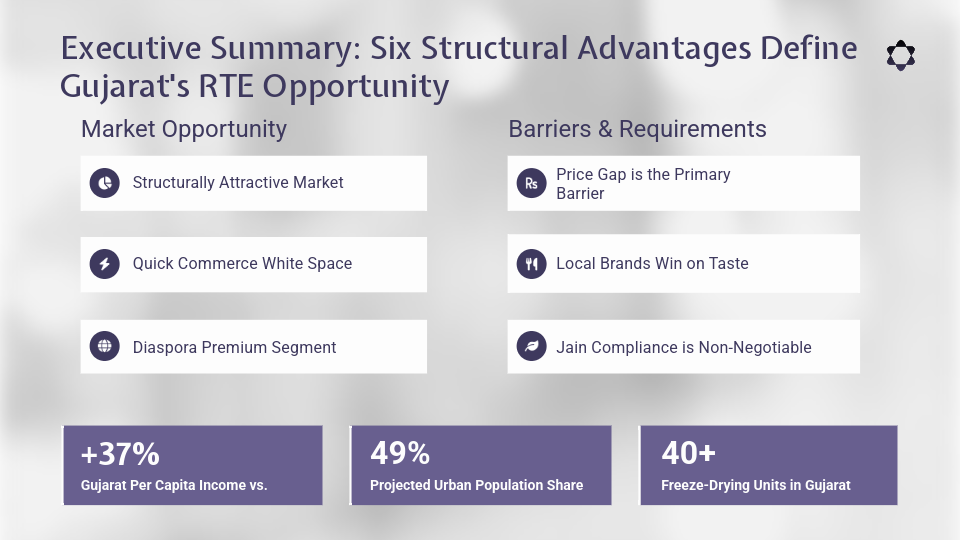

Gujarat RTE Market Report Freeze-Dried & Dehydrated Meals

Gujarat has emerged as a premier hub for the freeze-dried ready-to-eat (RTE) food industry, driven by per-capita income 37% above the national average and rapid urbanization. While the sector currently occupies a premium niche due to price disparities with traditional retort packaging, the state's advanced manufacturing infrastructure offers a clear path for asset-light market entry. Strategic opportunities are particularly concentrated in urban centers like Ahmedabad, where a significant "first-mover" window exists on Quick Commerce platforms (Blinkit, Zepto, and Swiggy Instamart) to capture the demand of time-constrained professionals. To win in the Western India food tech landscape, brands must bridge the gap between local flavor authenticity and national-scale reliability. Key growth drivers include strict adherence to Jain dietary compliance—a non-negotiable requirement for regional loyalty—and the untapped potential of the Gujarati diaspora which represents 33% of the total Indian diaspora worldwide. As global demand for lightweight, long-shelf-life ethnic meals rises, the export market represents a price-insensitive segment for authentic Gujarati cuisine. Success will belong to players who can optimize local contract manufacturing to challenge existing price barriers while dominating the digital shelf. You will get a PDF (4MB) file